The elevation of shareholders’ rights above the rights of all other stakeholders – patients, communities, customers, even the broader public – was not the result of random circumstances. It is the predictable outcome of agency theory, the management doctrine that took hold in the 1980s and redefined a manager’s ethical duty to owners alone. This worldview has become so normalized across the industrialized economy that its consequences are met with resignation, if not indifference, by the media and the public. Yet its effects on publicly funded care systems are profound and corrosive.

Agency theory is incompatible with humane publicly funded health care in general, but it manifests in its ugliest form in a nursing home setting. These facilities care for people who cannot advocate for themselves, whose well-being depends on labor-intensive, relational, time-consuming human attention. Under a shareholder-first model, those needs are inevitably subordinated to investor demands. As finance has shifted from supporting the mission of care to becoming the mission itself, the rights of residents have been incrementally and increasingly sacrificed to return on investment.

Attempt to reform the nursing home system is counterproductive for the simple reason that it sends messages that the system is a legitimate form of caring for the elderly and disabled. All that can be accomplished by tweaks is a false belief that the system will become fundamentally what citizens in a civilized society think it should be. That will not happen. The promise of reform becomes a kind of industry induced fantasy, reassuring the public that the system is on a path toward decency when it is structurally incapable of delivering it. In this way, reform does not challenge the system’s legitimacy; it reinforces it, allowing a fundamentally extractive model to masquerade as a form of care.

Rather than attack the illegitimacy of the system, advocates and the media look for bad actors who, they believe, could be eliminated for the purpose of transforming the current, normalized mode of organizing and caring for nursing home patients. By isolating the problem to a handful of villains, the public is encouraged to believe that the system can be redeemed once the “worst actors” are removed. But the very conditions that produce neglect, exploitation, and suffering result from the financial and organizational logic of the industry. The search for bad actors is a diversion that hides the underlying structure from scrutiny and allows the cycle of harm to continue uninterrupted.

These patterns reveal a system in which care “failures” are systemic and structural – not a system in need of better oversight or more competent operators. In reality, the nursing home industry as a whole is a tragic failure propped up by fantasies of total reform through democratic processes. Widespread dehumanizing care in the publicly funded long-term care system is the predictable result of organizing that care around financial extraction, opacity, and lack of accountability. As long as this model remains intact, no amount of reform will produce the dignity, safety, or freedom that a democratic society owes its elders and disabled citizens.

Confronting the reality of widespread abuse, neglect, and indignities is an act of political clarity and courage. It allows us to see that the crisis in long‑term care is not due to technical problems that can be tweaked away, but as civic failure—a question of what kind of society we intend to be. A democratic people cannot outsource care to a structure that negates the very conditions of democratic life: reciprocity, transparency, shared responsibility, and the possibility of new beginnings. The task before us is not to perfect an illegitimate system but to replace it with forms of care that honor human dignity and restore the bonds of democratic belonging.

Statement on the Presidential Pardon of Joseph Schwartz: A Symptom of Systemic Impunity in Long-Term Care

November 19, 2025

The presidential pardon of Joseph Schwartz, former owner of Skyline Healthcare, is not an isolated act of clemency—it is a clarion signal of a deeper institutional rot. Schwartz, who oversaw the collapse of a nursing home empire spanning 15 states and pleaded guilty to a $38 million payroll tax fraud scheme, has now been absolved not by the courts, but by executive fiat. This decision follows a disturbing trend: the repeated use of presidential pardons to shield nursing home executives from accountability, even as residents, workers, and taxpayers bear the cost of their misconduct.

Skyline’s implosion left a trail of unpaid workers, neglected residents, and shuttered facilities. Yet Schwartz is now the third major nursing home operator to receive clemency from President Trump, joining Paul Walczak and Philip Esformes—both convicted of large-scale fraud in the long-term care sector. These pardons send a chilling message: that financial crimes in elder care, no matter how vast or harmful, are ultimately negotiable.

This is not just a failure of justice—it is a failure of regulation. For years, federal and state agencies enabled Skyline’s expansion despite glaring red flags: undercapitalization, opaque ownership structures, and repeated violations. The Centers for Medicare & Medicaid Services (CMS) continued to reimburse Skyline even as facilities deteriorated. State licensing boards approved transfers to Schwartz’s control with minimal scrutiny. And when the collapse came, oversight agencies scrambled to contain the fallout rather than confront its systemic roots.

The pardon of Joseph Schwartz is a political act—but it is also a policy failure. It reflects a regulatory architecture that prioritizes corporate continuity over resident safety, and a justice system that too often distinguishes between criminality and consequence based on wealth and proximity to power.

We call on Congress, CMS, and state regulators to treat this moment not as a footnote, but as a flashpoint. We need:

Mandatory financial transparency for all nursing home owners and operators, including private equity and related-party entities.

Real-time enforcement mechanisms that prevent operators with histories of fraud or neglect from acquiring new facilities.

Federal legislation that bars individuals convicted of healthcare fraud from receiving executive clemency without congressional review.

A public reckoning with the structural incentives that allow profiteers to extract wealth from systems meant to protect the vulnerable.

The pardon of Joseph Schwartz is not the end of the story. It is a beginning—an opportunity to demand a system where care is not a commodity, and justice is not a privilege.

The American People Have a Right to KnowWhat They Are Getting for Their Hard-Earned Money– That’s Why We Formed the People’s Data Project (PDP) as a component of the Center for Health Information & Policy (a 501c3 nonprofit organization).

U.S. taxpayers and users of the government-corporate privatized healthcare system are paying 2 to 3 times as much as residents of peer countries such as England, Japan, South Korea, France, Canada, and all of the Scandinavian countries. While all residents of those countries have either free or affordable access to medical care, over 30 million Americans have no insured access to a doctor, clinic, or hospital. The uninsured either forego care or risk bankruptcy.

The ugliest facet of this disgrace is that the uninsured pay taxes for the care they are not getting. Indeed, the poor often pay more disproportionally because the states’ proportion of Medicaid is paid to a large degree with sales and property taxes, both of which are regressive. And yet it is the poor who are targeted for bureaucratic harassment and denial of services. We will be saying much more about this in the months and years ahead.

Ethical and moral issues are crucial in the fight against predatory corporate practices, but effectively opposing bad corporations and their executives requires valid and reliable data. For instance, the nursing home industry claims that pervasive neglectful care by Medicare and Medicaid-funded long-term care is justifiable due to inadequate Medicaid reimbursement. As we will demonstrate with overwhelming evidence, this is false. It is an intentional lie pushed through a powerful lobby (see post today: Nursing Home Industry Financial Propaganda is a Barrier to Decent Medicaid Funded Long-Term Care).

“Effectively opposing bad corporations and their executives requires valid and reliable data.”

The People’s Data Project: A Data Ecosystem for Healthcare Data Accessibility & Transparency

Americans intuitively know that the privatized healthcare system is siphoning off excess amounts of funding for their healthcare into the pockets of private interests. However, the only data available that people need and deserve to prove that their taxes, premiums, deductibles, and co-payments are unduly and excessively channeled from their care to investors and executives are rarely obtainable without the aid of advanced data analytical tools. For instance, hospital and nursing home cost report Public Use Files (PUFs) are available online.

One problem is that the files are too large to open in a commonly used spreadsheet. The data must be merged with other data files and converted into file formats suitable for analysis. Even when the data is analyzable in a typical spreadsheet, considerable assistance from data analysts who have experience with cost reports is necessary. That is the role and purpose of the People’s Data Project. We prepare and analyze data for nonprofit organizations, legislators, and other Americans who want to understand how money flows through nursing homes, hospitals, Medicaid contractors, and other providers of U.S. healthcare nationally, as well by region, state, county, city, and zip code.

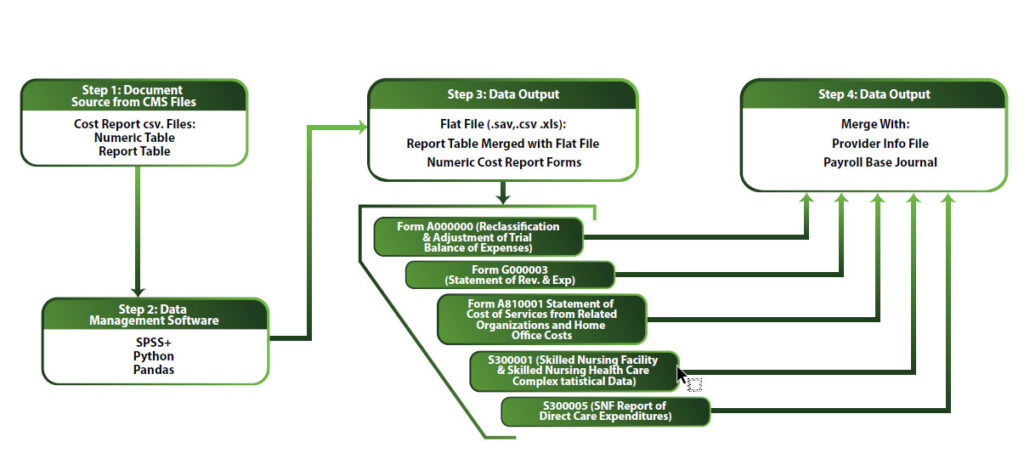

Our data ecosystem has been built with an IBM-SPSS statistical core using Python/Pandas programming languages for file transformation, analysis, and data modeling. Steps in the analytics of hospital and nursing home cost reports are depicted in the schematic below.

This schematic displays the originating sources of data, the tools used to format the data for creating needed output, the necessary organizing structure, and the files the with which data are merged to complete the full picture.

The PDP makes data available online usable for the lay public. In addition, we have extensive experience with and knowledge of hospital and nursing home data and other obtainable healthcare data. Our purpose is to assist nonprofit organizations, researchers, and lay people with obtaining and analyzing data within our bailiwick.

The Dangers of Predatory Corporate and Government Data Analytics are Creating a Democratic Crisis.

Without integrity in the collection and use of data by governments and corporations, Democracy as we know it will disappear. Unfortunately, the power of contemporary corporations with sophisticated technology is producing a crisis of citizen powerlessness. It is also unfortunate that too many professionals and politicians are indifferent to glaring conflicts of interest and intentional misinformation for the purpose of manipulating and misleading the public.

“Without integrity in the collection and use of data by governments and corporations, Democracy as we know it will disappear.”

The data crisis we are facing can only worsen with the advent of AI and increasingly sophisticated data analytics tools. It is despicable for industries to misuse technology and statistics to prey on unsuspecting populations needing healthcare. There is no doubt that AI is a powerful tool that can be used against “We the People.” However, The People’s Data Project will empower people to harness the power of AI and data analytics for fighting back against those forces that are using it against them.

Narratives Make a Huge Difference in Politics: The People’s Data Project (PDP) Will Debunk the Nursing Home Industry’s False Narrative

The nursing home industry, represented in Washington, D.C. and all 50 states by the American Healthcare Association, has been successful in pushing a simple narrative: “Nursing home companies are operating on a ‘thin margin’ due to inadequate Medicaid reimbursement; therefore, they can’t afford to provide adequate staffing and decent care.” This hardship plea has been successfully sold to politicians, the media, academics, and the public in general.

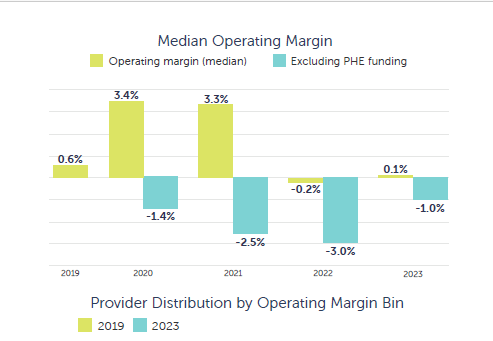

At the People’s Data Project, we have the data and the data analytic tools to debunk AHCA-funded misinformation. We will begin with the misleading annual report[i] put out by the major accounting firm of Clifton, Larson, & Allen (CLA) on behalf of the industry. The bar charts below appear in the accounting firm’s latest report. These graphics display the nursing home industry “Median Operating Margin” for 2023.

“From a financial and statistical perspective, the above presentation is highly flawed….”

From a financial and statistical perspective, this presentation is highly flawed and, for a leading accounting firm, disingenuous. We have the same data as CLA. We will show briefly in this post why the operating margin as referenced in the above graphic has no relevance to the important concept of “cash flow” – the flow of capital through a network of facilities onto the Income statements, “Cash Flow statements, and “Balance Sheets” of Parent Corporations. Rarely are nursing home facilities stand alone, independent subsidiaries with meaningful financial statements. Rather, they are conduits for cash to parent/holding companies.

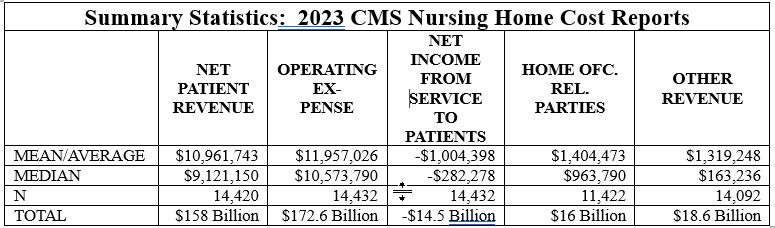

The PDP data files include data from cost reports submitted by 14,440 facilities for 2023. Net operating income in our file – displayed in the table below – is not significantly different than that reported by CLA.

Certainly, accountants at CLA know that foisting these statistics in this manner on an unsuspecting public is unethical. They are failing to add data and explanations that place them in proper perspective. The data are extremely skewed in a negative direction, which pulls the average and even the median in a negative direction. A skew of -38.33 is so extreme that point estimates are of no use when all the data is dumped into a stats package and no adjustment is made for the shape of the data.

But statistical validity problems such as skew aren’t the only problems with the way nursing home operating net is used in the industry narrative. Here are the major problems with operating net that CLA accountants most certainly understand:

Net operating income (net income from service to patients) is net patient revenue minus expenses. Expenses include payments to parent and holding companies of the facilities reporting net operating income (see the table below, which indicates $16 billion allocated to related parties and home office allocations).

Reimbursement from sources other than Medicaid/Medicare reimbursement and self-pay are not included in operating net income. However, as the table below indicates, other revenue for state incentive programs, COVID relief, and other sources totaled $18.6 billion in 2023 but is not added to the operating margin by CLA & AHCA.

Operating expenses of $172.6 billion include payouts to parent/holding companies for management fees of $16 billion. Also, other revenue from incentive programs, COVID relief, and other sources of $18.6 billion added to the net patient revenue, along with home office allocations and payments to related parties (subsidiaries owned by parent/holding companies) creates a different perspective than operating net.

When home office allocations, payments to related parties, and nonpatient revenue is added to net operating income, it appears that 12.7% of industry patient revenue is funneled to owners of nursing home chains. There are other sources of income for chain owners through tax write-downs for interest, taxes, and depreciation. In future posts, we will discuss other vehicles available to the nursing home industry for adding value to Medicare and Medicaid reimbursement.

Why Do We Have Character Tests for Medicaid Eligibility and Not for Any Other Government Subsidized Healthcare?

Medicaid is a $trillion-dollar program that has become a cash cow for the likes of UnitedHealth, Centene, Molina, Aetna, and Humana. At the same time, it has always been a badge of shame for the lowest income Americans needing care. Rules, regulations, and government oversight of the program are applied in the harshest of ways to poor people needing healthcare but not to the corporations responsible for widespread fraud and abuse.

Unlike major corporations funneling $billions in undeserved compensation to executives and generous returns to investors, Americans needing healthcare but too poor to qualify for other federally subsidized programs must prove to a state government that they are poor enough and of good enough character to get Medicaid. The stigma and harshness heaped on applicants and beneficiaries varies from state to state. For instance, the pious, holier-than-thou, Christian governor of Arkansas has been on a crusade to ferret out people in her state who, in her view, are unworthy of life saving medical care.

Who Deserves Quality Medical Care – or Any Medical Care for that Matter?

The concept of the “deserving poor” versus the “undeserving poor” has been integral in societal assistance for the economically unfortunate from the very beginning of North American colonization. Poverty has always been and still is considered a character flaw. It was just last week that I heard Mehmet Oz – the new overlord of Medicare and Medicaid – pontificated about – as he put it – “Abled bodied men,” who should not get Medicaid benefits if they are not suitably employed.

Most ordinary, non-superrich, Americans probably can’t conceive of the $trillions in government benefits handed to the wealthiest among us without a scintilla of concern about character. Think about a young, unemployed, able-bodied male who inherits $30 million from his parents. He will pay no taxes on that inordinate sum of money that he can use for his pleasure – and for concierge medicine. Maybe he is of good character, looking for work or contributing as best he can to society. Conversely, he may be into jet setting and partying without any intention of doing anything positive for society. However, the medical profession won’t consider any of that if he needs medical care.

The legislature in the State of Kansas, near where I live and do a considerable amount of work, refuses to expand the Medicaid program under the Affordable Care Act. Cross-wearing Christians in the state legislature believe that it’s some kind of a sin for the government to help poor people. They don’t give a second thought to the massive subsidization of agri-corporations, tax write-downs for the oil and gas industry, etc. They don’t seem to be concerned about the millions of acres of corn subsidized by the federal government at 50 cents per bushel while rich farmers and agri-corps irrigate it with water from the people’s Ogallala Aquifer, which is being depleted by such craziness.

There are countless instances of government benefits provided without concern for the worthiness of the beneficiaries. I grew up with farmers who loved the Soil Bank because they could let land lie fallow and collect a payment from the government. These farmers, with few exceptions, thought then and think now that welfare in the form of assistance to poor mothers for food, clothing and shelter is despicable.

Medicaid is an Inferior Healthcare Program Conceived by Southern Segregationists in the 1960s.

Medicaid is the handiwork of post-Reconstructionist Southern Democrats. Their sole purpose was to keep black people from getting medical care.[1] They were able to engineer and codify into law a unique American concept known as “indigent medical care.” The 1960 Kerr-Mills Act, ensured that the U.S. would have second-class medicine for the “needy” or “indigent,” and that state governments would have dominance over it.

Senators and Congressmen from the former Confederate States left the Democratic Party in the 1970s. Their political heirs in the current Republican dominated legislature and executive branch are now in the process of passing legislation that will further tilt the U.S. tax system in favor of the wealthy. They are attempting to enhance corporate and superrich tax advantages on the back of people needing medical care – medical care that the least fortunate amongst us can only get from Medicaid.

For obvious reasons, it has always been easy to politically bully poor people and, of course, poor black people are easiest of all to bully. We should also remember that the Southern States are not the only racist states. Furthermore, Medicaid in any state will be a second-class medical care program with inordinate amounts of fraud on the part of the companies contracting to provide services. Nevertheless, had there been no history of slavery, Jim Crow, and the ongoing institutional racism they have wrought, the U.S. healthcare system would look a lot more like our peer countries in Asia and Europe (where everyone has equal access to one national, medical care program).

It is Time to Get Honest and Give Everyone Equitable Access to Quality Medical Care

Medicaid is a disgraceful medical charade with roots in the incomprehensible cruelty of slavery and its aftermath. There is of course what critical race theory dubs intersectionality – white-, Hispanic-, Asian-, Native-poor people are caught up in it also. The results are these: poor black men will have 12 years less life to live than rich white men, the life expectancy of whites with a high school education or less has gone into reverse, black men die of cancer at a rate double any other demographic group, patients in hospitals on Medicaid are sicker, cost more, and stay longer than patients on any other payer system – just to list a few of the consequences of healthcare discrimination.

There has never been a time in American history when the rich lived longer with better health. On the other hand, there has never been a time when the bottom half of wealth holders and earners experienced a declining life expectancy and worse health outcomes compared to the fortunate upper classes.

The right wing and the medical industry are using a clever tactic by keeping us all bogged down in a fight over tweaking, improving, expanding a system that will never be anything other than means-tested, welfare medicine. Poor people’s medicine is and always will be inherently poor medicine. As long as the program exists, there will be an immoral distinction between the worthy and unworthy in the U.S. medical care system.

My question to the medical profession is this: “How do you square medical ethics with denial of care because a person can’t afford to pay or because some bureaucrat deems them unworthy?” I’m not berating individual doctors – I’m asking the medical profession, “Where in the hell have you been?” There are many good physicians that are in the fight to change the corrupt, discriminatory medical system. But this very powerful profession itself has a shameful track record in standing up for the human dignity of all people needing medical assistance.

End it! Don’t Mend It!

So, I say, the only solution to this American healthcare disgrace called Medicaid is “End it! Don’t Mend it.” Give everyone equal access to equitable healthcare. Fighting over nuances in a program unworthy of the fight keeps a white, college educated, advocacy enterprise going and ensures that the system itself won’t change. I see verbal assaults on bad nursing home chains, and on private equity in the hospital/nursing home industry, and other such ongoing battles as nothing more than a futile game of whack a mole that will be never ending. I’ve been playing that game. And I’m tired of it. The nursing home industry is fine with the game as is every other sector of the healthcare industry feasting off of government largesse like we could hardly imagine a half century ago.

[1] My interest in Medicaid research has been on systems analysis rather than the litany of bad acts by bad providers such as is the tenor of Mary Adelaide Mendelson’s wonderful and productive work Tender Loving Greed, which is a classic in the study of fraud and abuse in the nursing home industry. Systems research is focused on how systems originate, develop over time, and are politically maintained. The concept of “sensitive dependence on initial conditions” is critical for understanding why poor and African Americans are treated differently – and inequitably – in the healthcare system (See for instance, Walter Buckley, Sociology & Modern Systems Theory). For the best validation of the racist roots of Medicaid, see: Jill Quadagno, One Nation Uninsured: Why the U.S. Has No National Health Insurance; Gerard W. Byouchuk, National Health Insurance in the United States & Canada; and, Robert & Rosemary Stevens, Welfare Medicine in America: A Case Study of Medicaid.

A Medicaid Disgrace: Nursing Home Companies Make Big Bucks Off of Poor Peoples’ Medical Care

Medicaid expenditures by Federal and State governments are approaching $1 trillion per year. All of it has been privatized with hundreds of billions of public dollars funneled into the nursing home industry alone. That’s unfortunate because tax paying Americans pay dearly for privatized government services. While healthcare accounts for about one-fifth of U.S. GDP, peer countries spend half to one-third of that amount on much fairer and more effective government-administered healthcare systems.

It is important that we expose the excessive extraction of government funds from Medicaid by private companies and some nonprofit entities engaged in Medicaid contracting with states. Corporations such as Centene, UnitedHealth, Aetna, Humana and Molina have captured the bulk of primary, preventative, and acute care Medicaid contracts. They have an incentive to deny care and control their networks to keep their costs low. In upcoming posts, I will cover that facet of Medicaid.

Nursing home Medicaid contracting involves a conglomeration of LLCs, Real Estate Investment Trusts, Public Corporations, sole proprietorships, nonprofits, and private equity owned chains. It is a big industry with net patient revenue of approximately $200 billion. This does not include earnings from real estate, dietary services, labor contracting, and other services sold by parent/holding companies to the nearly 15,000 nursing home facilities in the U.S. For instance, in 2022, the total cost of dietary services noted as expenses in cost reports totaled $12 billion. This is a money maker because parent companies buy in bulk, negotiate a favorable deal, and charge their facilities – the state contracting entities – full price.

If You Have Seen One Nursing Home Chain, You Have Seen One Nursing Home Chain.

The nursing home industry is comprised of diverse legal, and financial structures run by a variety of characters and investing entities. Some of the characters have become quite notorious for accumulating great wealth while providing appalling care. A couple of the better-known investor/owners with unsavory reputations are Ephram Lahasky and Forrest Preston. Lahasky’s name appears in our research on ownership all over the United States. He’s been denied a license to operate by the state of Vermont and has been sued by the Attorney General of New York. Preston is the sole owner of one of the largest chains in the U.S. – The Life Care Centers of America. Both of these guys continue to run substandard nursing homes unabated. There are plenty others that are somewhat less noticeable but just as bad or worse.

Infamous operators aside, documents available regarding publicly listed companies provide the best insight into the industry’s extraction of taxpayers’ dollars that could otherwise be applied to decent and humane care as opposed to the warehousing care that is pervasive in the highly profitable nursing home business. There are financial advantages to companies listed on a stock exchange. Capital is available from investors through the sale of stock. If the stock price increases, so does the availability of capital for expansion, return to shareholders, and executive compensation.

In the right business, stock becomes attractive, appreciates, and provides a nice return. The nursing home business is the right business because taxpayers guarantee revenue and ensure robust net incomes that are shielded from ordinary business cycles and economic crises such as caused by the COVID pandemic.

The Ensign Group: $4.2 Billion in Medicaid & Medicare Nursing Home Business Per Year

The Ensign Group is one of the largest nursing home chains in the U.S. It is listed on the NASDAQ. The advantage of publicly listed companies to the taxpayers is transparency. Public companies are required to file financial statements with the Securities & Exchange Commission. CMS data and financial reports submitted to the SEC by the Ensign Group suggests that outstanding returns do not equate with high quality care.

As information from Ensign’s latest SEC 10K and Proxy Statements and data from the CMS ProviderInfo file suggests, this $4.2 billion corporation is making a handsome return on very poor-quality service. CMS Nursing Home Care Compare rates facilities on a scale of 1 to 5 with 1 being the lowest on a variety of factors such as nursing hours of care per resident day, turnover, patient care overall, and so forth. Of the 268 Ensign affiliated facilities in the July 2024 ProviderInfo file, 22% were rated 1 and 32% were rated 2 – only 1.5% were rated 5. So, over half of this company’s facilities are rated at the bottom in quality while their investors and executives are richly rewarded.

In view of Ensign’s appallingly low performance on care ratings, let’s look at the following financial data they reported to the SEC: (1) return on shareholder value, (2) stock repurchase, (3) cash on the balance sheet, (4) executive pay, and (5) net cash provided by operating activities. It is important to keep in mind that approximately half of the 56 million shares of stock are owned by three asset management firms BlackRock, Vanguard, and State Street.

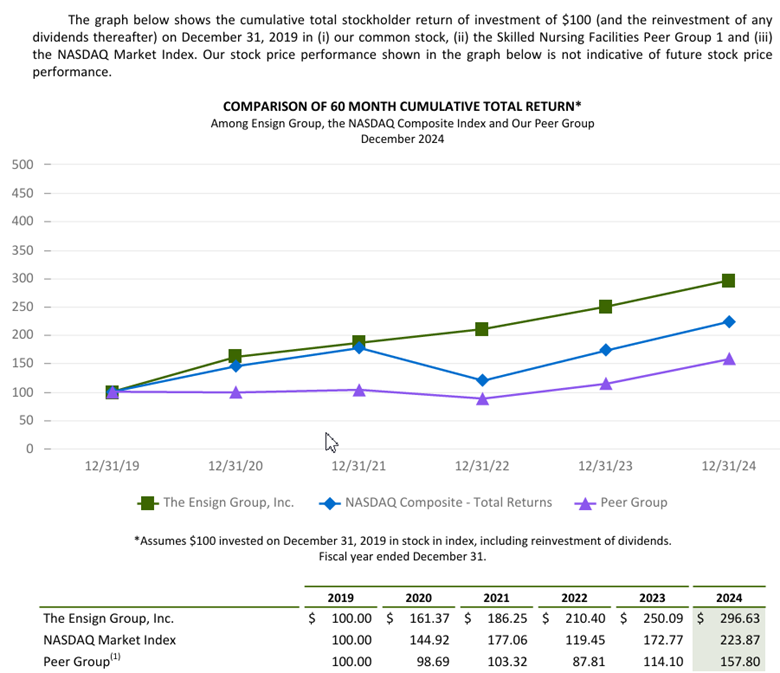

$100 Invested in Ensign in 2019 was worth $296 at the end of 2024.

The Ensign Groups 10K touts the company’s cumulative stockholder return from 2019 through 2024 per $100 invested in 2019. The chart below indicates that Ensigns outperformed the NASDAQ Composite and peer companies. A $100 dollar in 2019 was worth $296.63 in 2024.

Stock buybacks drain money from production/service and raises the price of stock.

Ensign noted in its financial report that it invested $20,000,000 in a stock buyback in 2024. Stock buybacks raise the price of the stock and enrich shareholders and executives. Money that could be reinvested in business operations and improved care is extracted for the purpose of rewarding investors. Investors have indeed been quite positive toward Ensign stock. When the market tanked in November of 2021 due to COVID and the Federal Reserve’s monetary tightening, Ensign stock was selling at $75 per share. Today it is trading at over $140 per share.

Don’t believe industry propaganda – nursing homes are not “running on a thin margin.”

Ensign’s 2024 cash flow statement notes net cash from operating activities of $324 million. Their balance sheet indicates cash and cash equivalents of close to a half billion dollars ($464,598 million).

Executives are richly rewarded for impressive financial performance and disgraceful performance on their contract with taxpayers.Five top executives’ compensation totaled $110 million over 3 years.

As the table below demonstrates, the compensation of Ensign’s five corporate executives totaled nearly $110 million over the past three years. It is notable that actual salary for all of the top executives/officers are less than $1 million while their total compensation ranges from $4 to over $11 million per year. Corporations receive a tax advantage for keeping executive salary below $1 million and putting the bulk on stock awards, stock options, bonuses, and perks. Therefore executives have an incentive to keep costs (services) low and poor while increasing shareholder value.

Summary

Data pertaining to one large nursing home chain only scratches the surface of the financial reality of privatized, government sponsored, healthcare in America. The initial purpose of Medicaid was to keep states in control of government funded medical care for poor people. Throughout the 1940s, 50s, and 60s, bigoted Southern Democrats had outsized legislative power to block a single payer, universal healthcare system managed by the federal government. Their goal was to keep African Americans in an inferior position. They were able in the 1940s to include a segregation clause in the Hill-Burton Hospital Survey & Construction program and block President Truman’s plan for single-payer, universal medical care.

After Truman’s fight for equitable healthcare along the lines of programs adopted by European governments and countries with advancing economies in Asia, the Democrats gave up and went along with a “Rube Goldberg” government healthcare system designed to discriminate against black Americans and enhance the power of states over the federal government in the realm of medical care. Consequently, American government sponsored medicine became divided along race and class lines. That did not stop venal politicians from pouring increasing amounts of taxpayer dollars into Medicaid and turning it into a cash cow for their corporate patrons.

Note: The Ensign Groups 10K and Proxy Statements can be found here: The Ensign Group, Inc. – Financials – SEC Filings. The CMS ProviderInfo file is available on the CMS website or through a request to dkingsley@tallgrasseconomics.org.

Everyone But the Totally Uninsured Receives Government Subsidized Medical Care. Only the Poor are Stigmatized

Practically all medical care in the U.S. is subsidized by federal and state governments – mostly by the federal government. The taxes to pay for these subsidies are collected from workers’ paychecks, sales taxes on what they buy, and property taxes that are paid by homeowners or added into rent/lease payments. And yet, it is only Medicaid, a medical care program for the poor, that is stigmatized. But the poor pay taxes too. Indeed, a disproportionate share of taxes.

The biggest tax subsidy is awarded to companies providing health insurance for their employees. When companies can write down their federal income taxes, they are actually getting money from the government – they are legally allowed to keep money that they owe the government. That is why these “breaks” are called tax expenditures.

Indeed, the $251 billion in tax write downs for corporations providing health insurance is the largest tax expenditure by far.[1] Furthermore, this deduction is a transfer of wealth from lower income Americans (who earn their employee benefits) to wealthier classes who increase their assets from equities and compensation in the healthcare industry. In costing labor, employers trade benefits for wages. In fact, in many negotiations in which I was on the negotiating team, we often settled wage disputes by offering to “sweeten the health insurance package.”

The poor pay more than their fair share of taxes that keep governments running. In the U.S. taxes on capital have been continuously reduced while at the same time taxes on consumption and labor have increased. This puts the heaviest burden on the lowest income groups and lightens higher income groups’ tax load. Nevertheless, Medicaid recipients are treated like freeloaders and “lesser thans” while everyone receiving other forms of subsidized healthcare are considered solid, upstanding Americans by politicians blaming poor people and the elderly for budget deficits.

“What We Do unto the Least of These”

Capitalist America as it has evolved can be harsh and unforgiving for the unfortunate, which could be any of us. With job loss, we can find ourselves struggling to keep a roof over our head and food on the table. At the very least we could lose our health insurance. The Affordable Care Act is not affordable for the unemployed. If you live in a state that has not expanded Medicaid, i.e., has not made residents with incomes below 120% of poverty eligible for Medicaid, you must have children and be in extreme poverty to qualify. If not, you will not be eligible for any healthcare program.

Let’s say a person lives in a state that has expanded Medicaid. And let’s say that person lives in a so-called “red state” like Arkansas or Missouri. The governors and legislators of those states will humiliate them and create administrative barriers to establishing eligibility for no other reason than they assume they are a cheater until they prove otherwise. These legislatures are dominated by pious Christians who despise poor people despite their prophet’s admonishment “what you do unto the least of these; you do unto me.” It is easy to bully poor people for the purpose of impressing constituents with bravado about controlling wasteful spending.

The poor are despised by right-wing politicians and a large portion of Christian America. Certainly, we don’t see the powerful Christian Church Industry – otherwise known as “faith based” institutions – closing ranks to take up the cause of their less fortunate brethren. Their prophet did that but for the most part they seem reticent about exerting their influence.

Transfer of Wealth from the Poor to the Wealthy

Conservatives claim that poverty in the U.S. is far lower than officially measured by the federal government due to transfer in the form of welfare such as Medicaid, child tax credits, and the Earned Income Tax Credit. There are several problems with the conservative wealth transfer argument. First, the poor struggle day-to-day to survive due to paltry benefits and continued threats of loss of those benefits and actual loss due to administrative complexities that are hard to navigate in a hostile political environment.

Second, transfers to the poorest of the poor are paltry compared to the transfers to the upper classes in the form of such mechanisms as capital gains write downs, untaxed cash flow, earnings on unrealized gains, and investments in tax free municipal bonds – to name a few “loopholes” for the rich. The hypocrisy of politicians claiming to save “we the people” money by bullying poor people on Medicaid is palpable in legislatures these days. Congresswoman Vicki Hartzler of Missouri is a wealthy owner of an Agri Corp that receives hundreds of thousands of dollars in undeserved federal farm subsidies. Nevertheless, she is a loud voice for clamping down on benefits for the voiceless, the powerless, and the defenseless who need those benefits for their health and often for their very survival.

WATCH FOR UPCOMING BLOG POSTS:

“Lucrative Medicaid Funded Nursing Home Care”

“Finding the Roots of Medicaid in the History of Slavery & Jim Crow”

“Corporate Medical Care Benefits: The Privatization of Medicaid”

“The Poor as a Government Healthcare Class: A Uniquely American Idea”

“The Injustice of the ‘120% of Poverty Gap’ in States That Have Not Expanded Medicaid”

[1]Tax Expenditures | U.S. Department of the Treasury. Other big tax expenditures include the mortgage interest deduction, and a variety of corporate real estate write downs, including depreciation. There is no doubt that the tax codes are a major factor in the maldistribution of wealth.

YOUR FREEDOM, HEALTH & WELFARE DEPEND ON RESPECT FOR THE U.S. CONSTITUTION AND A GOVERNMENT THAT WILL ENFORCE IT

By:

Dave Kingsley

Without Government You are Without Protection from Self-Serving Corporations, Techno-Plutocrats like Musk, and Fascists.

Thanks to both major political parties, a phony government hating movement has been able to fester and eventually capture the levers of power in the United States. Indeed, hating government is fashionable these days. A shallow, faddish, libertarian political philosophy – unleashed by a doltish President in 1980 – has become de regueur.

A public distracted by trash entertainment has been moved by corporate media’s penchant for disseminating misinformation (e.g., Social Security has created a huge budget problem) as well as political propaganda (e.g., asylum seeking immigrants are a threat) to put a self-serving oligarchy in control. A very potent government hating, financier-industrialist led political apparatus has incrementally managed to engage major “news” outlets and political parties in furtherance of their economic interests at the expense of the freedom, welfare, and health of the very people who voted their candidate into office.

Blaming Social Security, Medicare, programs for poor people, economic equity/DEI, and the like is a scurrilous but effective mantra for promoting a “government bad, corporation good” narrative. Ronald Reagan instilled that incantation in the body politic throughout his eight years as president with little opposition from the Democrats. By the time the next Democrat ascended to the Presidency in 1992, the Democratic Party – now the “New Democrats” – were on board with the Reaganism and Ayn Randism that had taken hold. President Clinton said that the “era of big government is over.” What he meant was that poor people needed some tough love and that cutting safety net benefits and Social Security would be one way to carry that out. Enough Democrats were all in on that to change grants-in-aid to block grants that would allow state governments to humiliate and abuse poor people.

The Clinton Administration – with prodding from the venomous Newt Gingrich – did cut Social Security through a devious, back-door means. Conservative economists were put in charge of a commission – the Boskin Commission – that promoted and eventually won the day for recalculating the SS cost of living increases, which dampened the increases in monthly payments to beneficiaries. Along with both parties’ support of Reagan in pushing back eligibility for full benefits by two years – a massive cut – the statistically invalid reconfiguration of COLA increases insured that life would be harder for the majority of SS beneficiaries.

The next Democratic President, Barack Obama, tried to give away massive cuts to Social Security and Medicare but was rebuffed by the Republicans who thought he wasn’t giving quite enough away. Or perhaps they really thought that the Democrats could sell it as some kind of victory. So, the feckless and weak Democrats, garnering little respect from the masses, blamed Jill Stein for their loss in 2016, which is rather silly when you think about it.

Radical Government Haters and the Reductio Ad Absurdum

Now the government haters are in control and taking government hating to its logical conclusion. Sociopathic, narcissistic billionaires have been handed the right to dismantle the portion of our federal government that protects us from them and the fascists beholden to them. The real power now resides with super-rich techno-plutocrats such as Thiel, Bezos, Musk, and others who are in control of the entire digital communications infrastructure and, in cooperation with government, are sucking up information without regard to 4th Amendments rights against search and seizure. It was their data capabilities that allowed them to hand the last election to Trump.

Industrial behemoths such as UnitedHealth, Exxon, CVS, Walmart, Chevron, Monsanto/Bayer, and others now have an opening to achieve extreme deregulation, monopolistic market power (price fixing), excessively low to no taxes, and the right pollute our air, water, food, and building/manufacturing materials with toxic chemicals conducive to poor health and a shorter life expectancy.

Because of theocratic fascists of the Baptist, Catholic, and the “get down, holy rolling fundamentalist, government hating” varieties, the 1st Amendment separations of church and state provision of the constitution is in tatters. Attacks on 1st Amendment freedom of speech rights have intensified in the form of public policy (e.g., attacks on media outlets and journalists by Trump). Members of Congress who speak out are threatened and harassed. The few courageous House and Senate members who do speak out are sort of hanging out there alone. For instance, Congressman Eric Swalwell and his family have been going through hell while so many of his fellow Democrats stay in hiding and maintain a low profile.

Overwhelmingly, the elected representatives in both parties are cowards willing to slink into hiding rather than incur the wrath of a psychopathic President. Senate Minority Leader Schumer maintains that the Democrats can just wait for Trump to sink and the public polls to turn against him. Unfortunately, most Democrats have been relying on opinion polls for decades rather than standing up for what they believe.

It Will Get Worse Unless We Can Change the Democratic Party

Life expectancy will continue to move backwards as the plutocratic wrecking crew continues to disassemble the government and protections we rely on for a healthier life and environment. The people in power now care about only this: money and power. To the people running the U.S. today, the masses are merely fodder to be manipulated and fleeced. Those government services for which the middle and lower income strata pay disproportionately will be taken away for the purpose of enriching the rich.

Yesterday, a mass mailing from Democratic House Leader Hakeem Jeffries arrived in my mailbox. It was actually an appeal for money, which seems to be the main activity of the Democratic Party these days. This is the first paragraph verbatim:

“The American people deserve leaders who set aside partisanship and focus on bipartisan solutions. House Democrats are committed to working with the other side of the aisle to make life better for hardworking middle-class families. At the same time we will push back against their extremism whenever necessary.”

Just how delusional can a Democratic Party leader be? Since 1980 and the right-wing revolutionary regime of Ronald Reagan, bipartisanship has meant “Democrats rolling over.” Pushing back has meant “making some noise and then caving in to Republican demands.” Let’s take the massive 1983 bipartisan cuts in Social Security as an example. As a result of the Establishment’s stewing and fretting over funding the coming retirement of the Baby Boomer generation, eligibility was pushed back two years. There appeared to be no consideration of raising the cap and making the affluent classes pay a little more. That was the result of a recommendation from the “bipartisan” Greenspan Commission and an accommodative bipartisan vote in Congress.

Perhaps one could find a little bit of bipartisanship and Democratic Party pushback on extremism in the early days of the Reagan Revolution. But these days we are not talking about extremism of the Reagan variety. Over the past 45 years, extremism has evolved into a current regime of fascists, and neo-Nazi sympathizers intent on bringing back second-class citizenship for women, people of color, and gay people. They are also intentionally heaping cruelty on transgender, poor, and asylum-seeking immigrants. We are talking about a typically sadistic, fascist movement rife with anti-Semitism.

We now have in America a proclaimed dictatorship in league with the regimes of Pinochet, Franco, Salazar, and Mussolini. It appears that their leader thinks that Hitler had some good ideas. Of course, Washington Democrats along with their pals in the mainstream media aren’t pushing the current Republican’s self-anointed dictator to specify exactly what those ideas are.

Until recently, Republicans at least had a modicum of respect for the U.S. Constitution. But in January of 2021, an insurrectionist mob attacked the U.S. Capitol. Members of law enforcement were injured and some died as a result of the violence heaped on them. I watched in horror as goons wearing t-shirts with “Six Million Was Not Enough,” “Camp Auschwitz” and the like broke windows, assaulted police offices, and set up a gallows for the execution of Vice President Pence who refused to override the election results.

Eventually, many were convicted and held accountable. But now the U.S. dictator wannabe with support of his Republic sycophants in Congress have given them a pardon. These are the same leaders who have a rubber stamp Supreme Court that will back their destruction of all facets of federal government designed to protect and improve the lot of “we the people.” Project 2025 is designed for the betterment of the extremely wealthy. It will not end well for everyone else.

Where exactly does Congressman Jeffries see an opportunity for bipartisanship? This is a fanatical Republican Party that denied President Obama his constitutional right to select a Supreme Court Justice.

One give away regarding the state of the Democratic Party at the top these days is Leader Jeffries statement that the party wants to “make life better for hardworking middle-class families.” That’s laudable. However, life has become unbearable for low-income families in America. The Republicans are intent on slashing Medicaid, SNAP, and other programs barely keeping a large part of the U.S. population alive.

All of this will not end well for anyone in the U.S. except billionaires who can always seek refuge in more comfortable surroundings located far from the boundaries of the United States. If the Democratic Party continues its mealy-mouthed nonsense about bipartisanship and fails to operate (fight) from clearly stated principles, they will continue to sink and take the rest of us with them.

The data analytics system we have developed at the Center for Health Information & Policy (CHIP) – our nonprofit research organization – gives us the capability to drill into our extensive data on the nearly 15,000 skilled nursing and long term care facilities in the U.S. We feel confident that we have identified the bottom of the bottom dwellers and need to bring them to the attention of other professionals and the public. We are curious about why a chain like the one described in this post is allowed to operate with impunity.

RELIANT HEALTH CARE, LLC: AN EXTREMELY LOW PERFORMING MISSOURI NURSING HOME CHAIN

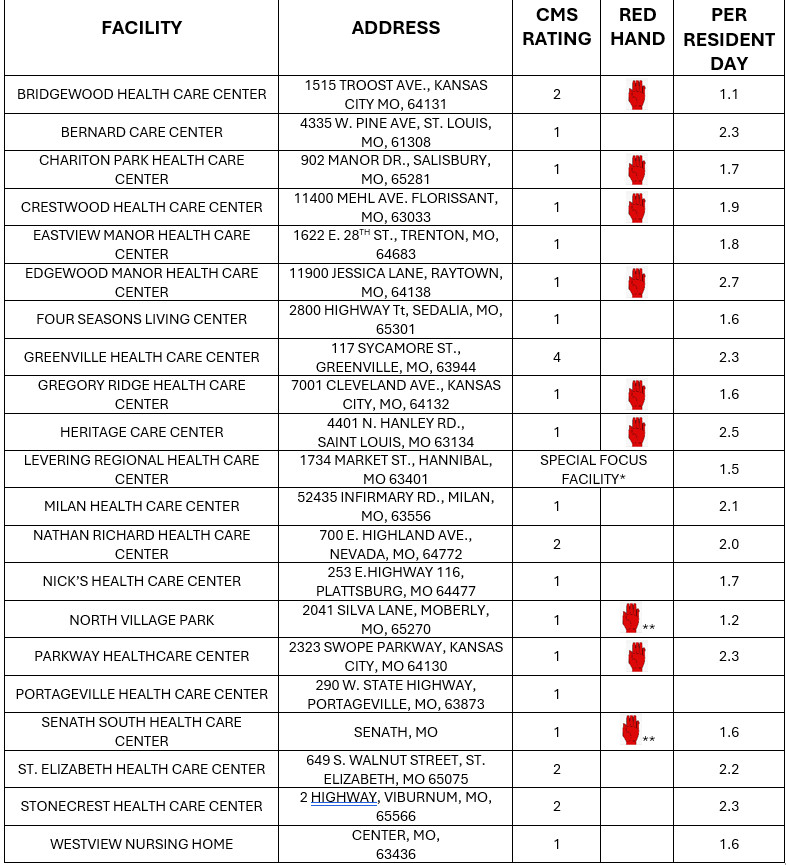

Reliant Care Management, LLC owns 21 Medicare & Medicaid funded skilled nursing facilities in the State of Missouri – four are in the Kansas City Metropolitan Area. In our work across the United States in cities, counties, states, and regions, we have not encountered a chain with lower federal ratings on quality of care. In this alert, we will lay out the case for a high level of concern among families, ministers, social workers and others who might have an occasion to find a skilled nursing facility for a loved one or a client.

LOOK FOR THE RED HAND

The Center for Medicare & Medicaid Services as the federal regulatory agency for Medicare and Medicaid funded skilled nursing has a complicated rating system for each facility that ranges from l for low performing facilities to 5 for high performing facilities. Facilities with a rating plus a red hand have incidents that present a danger to patients. It is rare for a chain of even a few facilities to have more than one red hand. Nevertheless, of the 21 Reliant facilities 9 have a red hand (see table below).

Red hands are signs of poor quality of care. In addition to incidents that place patients in immediate jeopardy, ongoing neglect often occurs due to a lack of adequate staffing. Nursing staffing is measured by the number of nursing hours per resident day (HPRD). The current average of the 14,516 skilled nursing facilities in our data file is 3.8 (3 hours & 48 minutes) HPRD for RN, LPN, and CNA staffing – which most experts agree is far too low. Nevertheless, nursing homes with an HPRD of 2 or less are quite rare – only 7 tenths of 1 percent or 103 out of 14,516 facilities.

As the table below illustrates, the hours per resident day column indicates that Reliant facilities are extremely understaffed (“HOURS” was somehow deleted from the column – it should be “HOURS PER RESIDENT DAY”). Indeed, HPRDs in the low 2s and 1s for an entire chain is appalling.

*According to CMS, a Special Focus Facility has, “More problems than other nursing homes (about twice the average number of deficiencies),” More serious problems than other nursing homes,” and “A pattern of serious problems that have persisted over a long period of time.”

**Special Focus Candidates:” Not quite bad enough to be a Special Focus Facility yet but moving in that direction. It is truly phenomenal to see a chain of this size with one SFF and two SFF candidates.

THE NURSING HOME CLASS DIVIDE AND THE RELIANT BUSINESS MODEL

If you’ve seen one nursing home, you’ve seen one nursing home. If you’ve seen one nursing home chain, you’ve seen one nursing home chain. If you’ve seen one state nursing home system, you’ve seen one state nursing home system. Nevertheless, similarities in patterns and practices can be seen in the SKN/LTC system. For instance, some chains accept Medicare but not Medicaid, some accept Medicaid and Medicare, some have very little Medicaid while others have mostly Medicaid as a payor. The amount of contract labor used, and the price paid for it varies from chain to chain and so forth.

With 90 percent of its bed days reimbursed by Medicaid, Reliant has an extremely high number of patients who are in long-term care and too poor to pay out of pocket. The company runs mostly large facilities (120-250 beds) and a small proportion of small facilities (approximately 60 beds).Bed size varies between and within chains. However, the pattern we see is this: the larger facilities in number of beds tend to be in poorer neighborhoods and serve a disproportionate number of Medicaid patients. We have also noticed that these “big” facilities with mostly Medicaid bed days tend to be rated lower in CMS Nursing Home Care Compare quality measurement system.

Some Significant Reliant Financial Information:

Average bed size of 113.5 (versus 90 nationwide but Reliant has a mix of a few small and very large facilities).

Patient revenue: $161.6 million

Net operating income: $3.3 million

Payments to Home Office & Wholly Owned Subsidiaries: $28.8 million

Reliant owned businesses supplying goods and services: management, therapy, pharmaceuticals, medical supplies, laundry subsidiaries (real estate side of the business is unknown at this time due to a lack of information)

All therapy services are contracted out to Reliant owned therapy subsidiary

Reduced labor costs through extreme low staffing and below average wages

WHO OWNS RELIANT CARE MANAGEMENT, LLC AND WHAT ARE OFFICIALS AND AUTHORITIES DOING ABOUT THIS CHAIN?

According to CMS ownership records, Reliant is owned by one individual – Mr. Rick DeStefane (see, e.g.: Find Healthcare Providers: Compare Care Near You | Medicare). Information (perhaps PR and propaganda) about Mr. DeStefane can be found on the Reliant website (Rick DeStefane | Reliant Care Management, LLC | St. Louis). We cannot be a judge of Mr. DeStefane’s character. We can only ask why his SKN/LTC facilities are rated lower than even some of the most scurrilous chains we have analyzed.

We would also ask Mr. DeStefane to show the taxpaying public Reliant’s consolidated financial reports, e.g. income statement, balance sheet, and cash flow statement. We have no idea the extent of personal wealth accruing to Mr. DeStefane and his family’s assets but we believe that the public has the right to know. Our federal and state governments have failed the public by allowing nursing home providers to hide their finances.

What are Missouri and federal legislators and regulators planning to do about Reliant? Are they even tuned into the ratings discussed in this bulletin? What are local politicians, health departments, ministerial alliances, and other individuals and organizations with an obligation to protect the vulnerable aging and disabled populations with a need for institutional nursing care doing about Reliant? Certainly, it is not OK to allow nursing homes this bad to operate below the radar.