By:

Dave Kingsley

A Medicaid Disgrace: Nursing Home Companies Make Big Bucks Off of Poor Peoples’ Medical Care

Medicaid expenditures by Federal and State governments are approaching $1 trillion per year. All of it has been privatized with hundreds of billions of public dollars funneled into the nursing home industry alone. That’s unfortunate because tax paying Americans pay dearly for privatized government services. While healthcare accounts for about one-fifth of U.S. GDP, peer countries spend half to one-third of that amount on much fairer and more effective government-administered healthcare systems.

It is important that we expose the excessive extraction of government funds from Medicaid by private companies and some nonprofit entities engaged in Medicaid contracting with states. Corporations such as Centene, UnitedHealth, Aetna, Humana and Molina have captured the bulk of primary, preventative, and acute care Medicaid contracts. They have an incentive to deny care and control their networks to keep their costs low. In upcoming posts, I will cover that facet of Medicaid.

Nursing home Medicaid contracting involves a conglomeration of LLCs, Real Estate Investment Trusts, Public Corporations, sole proprietorships, nonprofits, and private equity owned chains. It is a big industry with net patient revenue of approximately $200 billion. This does not include earnings from real estate, dietary services, labor contracting, and other services sold by parent/holding companies to the nearly 15,000 nursing home facilities in the U.S. For instance, in 2022, the total cost of dietary services noted as expenses in cost reports totaled $12 billion. This is a money maker because parent companies buy in bulk, negotiate a favorable deal, and charge their facilities – the state contracting entities – full price.

If You Have Seen One Nursing Home Chain, You Have Seen One Nursing Home Chain.

The nursing home industry is comprised of diverse legal, and financial structures run by a variety of characters and investing entities. Some of the characters have become quite notorious for accumulating great wealth while providing appalling care. A couple of the better-known investor/owners with unsavory reputations are Ephram Lahasky and Forrest Preston. Lahasky’s name appears in our research on ownership all over the United States. He’s been denied a license to operate by the state of Vermont and has been sued by the Attorney General of New York. Preston is the sole owner of one of the largest chains in the U.S. – The Life Care Centers of America. Both of these guys continue to run substandard nursing homes unabated. There are plenty others that are somewhat less noticeable but just as bad or worse.

Infamous operators aside, documents available regarding publicly listed companies provide the best insight into the industry’s extraction of taxpayers’ dollars that could otherwise be applied to decent and humane care as opposed to the warehousing care that is pervasive in the highly profitable nursing home business. There are financial advantages to companies listed on a stock exchange. Capital is available from investors through the sale of stock. If the stock price increases, so does the availability of capital for expansion, return to shareholders, and executive compensation.

In the right business, stock becomes attractive, appreciates, and provides a nice return. The nursing home business is the right business because taxpayers guarantee revenue and ensure robust net incomes that are shielded from ordinary business cycles and economic crises such as caused by the COVID pandemic.

The Ensign Group: $4.2 Billion in Medicaid & Medicare Nursing Home Business Per Year

The Ensign Group is one of the largest nursing home chains in the U.S. It is listed on the NASDAQ. The advantage of publicly listed companies to the taxpayers is transparency. Public companies are required to file financial statements with the Securities & Exchange Commission. CMS data and financial reports submitted to the SEC by the Ensign Group suggests that outstanding returns do not equate with high quality care.

As information from Ensign’s latest SEC 10K and Proxy Statements and data from the CMS ProviderInfo file suggests, this $4.2 billion corporation is making a handsome return on very poor-quality service. CMS Nursing Home Care Compare rates facilities on a scale of 1 to 5 with 1 being the lowest on a variety of factors such as nursing hours of care per resident day, turnover, patient care overall, and so forth. Of the 268 Ensign affiliated facilities in the July 2024 ProviderInfo file, 22% were rated 1 and 32% were rated 2 – only 1.5% were rated 5. So, over half of this company’s facilities are rated at the bottom in quality while their investors and executives are richly rewarded.

In view of Ensign’s appallingly low performance on care ratings, let’s look at the following financial data they reported to the SEC: (1) return on shareholder value, (2) stock repurchase, (3) cash on the balance sheet, (4) executive pay, and (5) net cash provided by operating activities. It is important to keep in mind that approximately half of the 56 million shares of stock are owned by three asset management firms BlackRock, Vanguard, and State Street.

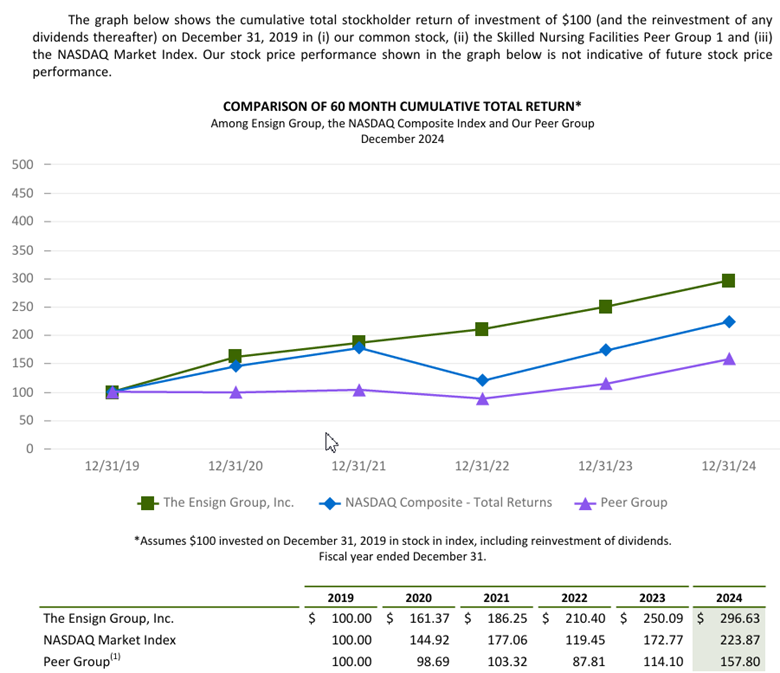

$100 Invested in Ensign in 2019 was worth $296 at the end of 2024.

The Ensign Groups 10K touts the company’s cumulative stockholder return from 2019 through 2024 per $100 invested in 2019. The chart below indicates that Ensigns outperformed the NASDAQ Composite and peer companies. A $100 dollar in 2019 was worth $296.63 in 2024.

Stock buybacks drain money from production/service and raises the price of stock.

Ensign noted in its financial report that it invested $20,000,000 in a stock buyback in 2024. Stock buybacks raise the price of the stock and enrich shareholders and executives. Money that could be reinvested in business operations and improved care is extracted for the purpose of rewarding investors. Investors have indeed been quite positive toward Ensign stock. When the market tanked in November of 2021 due to COVID and the Federal Reserve’s monetary tightening, Ensign stock was selling at $75 per share. Today it is trading at over $140 per share.

Don’t believe industry propaganda – nursing homes are not “running on a thin margin.”

Ensign’s 2024 cash flow statement notes net cash from operating activities of $324 million. Their balance sheet indicates cash and cash equivalents of close to a half billion dollars ($464,598 million).

Executives are richly rewarded for impressive financial performance and disgraceful performance on their contract with taxpayers. Five top executives’ compensation totaled $110 million over 3 years.

As the table below demonstrates, the compensation of Ensign’s five corporate executives totaled nearly $110 million over the past three years. It is notable that actual salary for all of the top executives/officers are less than $1 million while their total compensation ranges from $4 to over $11 million per year. Corporations receive a tax advantage for keeping executive salary below $1 million and putting the bulk on stock awards, stock options, bonuses, and perks. Therefore executives have an incentive to keep costs (services) low and poor while increasing shareholder value.

Summary

Data pertaining to one large nursing home chain only scratches the surface of the financial reality of privatized, government sponsored, healthcare in America. The initial purpose of Medicaid was to keep states in control of government funded medical care for poor people. Throughout the 1940s, 50s, and 60s, bigoted Southern Democrats had outsized legislative power to block a single payer, universal healthcare system managed by the federal government. Their goal was to keep African Americans in an inferior position. They were able in the 1940s to include a segregation clause in the Hill-Burton Hospital Survey & Construction program and block President Truman’s plan for single-payer, universal medical care.

After Truman’s fight for equitable healthcare along the lines of programs adopted by European governments and countries with advancing economies in Asia, the Democrats gave up and went along with a “Rube Goldberg” government healthcare system designed to discriminate against black Americans and enhance the power of states over the federal government in the realm of medical care. Consequently, American government sponsored medicine became divided along race and class lines. That did not stop venal politicians from pouring increasing amounts of taxpayer dollars into Medicaid and turning it into a cash cow for their corporate patrons.

Note: The Ensign Groups 10K and Proxy Statements can be found here: The Ensign Group, Inc. – Financials – SEC Filings. The CMS ProviderInfo file is available on the CMS website or through a request to dkingsley@tallgrasseconomics.org.