By: Dave Kingsley

The American People Have a Right to Know What They Are Getting for Their Hard-Earned Money – That’s Why We Formed the People’s Data Project (PDP) as a component of the Center for Health Information & Policy (a 501c3 nonprofit organization).

U.S. taxpayers and users of the government-corporate privatized healthcare system are paying 2 to 3 times as much as residents of peer countries such as England, Japan, South Korea, France, Canada, and all of the Scandinavian countries. While all residents of those countries have either free or affordable access to medical care, over 30 million Americans have no insured access to a doctor, clinic, or hospital. The uninsured either forego care or risk bankruptcy.

The ugliest facet of this disgrace is that the uninsured pay taxes for the care they are not getting. Indeed, the poor often pay more disproportionally because the states’ proportion of Medicaid is paid to a large degree with sales and property taxes, both of which are regressive. And yet it is the poor who are targeted for bureaucratic harassment and denial of services. We will be saying much more about this in the months and years ahead.

Ethical and moral issues are crucial in the fight against predatory corporate practices, but effectively opposing bad corporations and their executives requires valid and reliable data. For instance, the nursing home industry claims that pervasive neglectful care by Medicare and Medicaid-funded long-term care is justifiable due to inadequate Medicaid reimbursement. As we will demonstrate with overwhelming evidence, this is false. It is an intentional lie pushed through a powerful lobby (see post today: Nursing Home Industry Financial Propaganda is a Barrier to Decent Medicaid Funded Long-Term Care).

“Effectively opposing bad corporations and their executives requires valid and reliable data.”

The People’s Data Project: A Data Ecosystem for Healthcare Data Accessibility & Transparency

Americans intuitively know that the privatized healthcare system is siphoning off excess amounts of funding for their healthcare into the pockets of private interests. However, the only data available that people need and deserve to prove that their taxes, premiums, deductibles, and co-payments are unduly and excessively channeled from their care to investors and executives are rarely obtainable without the aid of advanced data analytical tools. For instance, hospital and nursing home cost report Public Use Files (PUFs) are available online.

One problem is that the files are too large to open in a commonly used spreadsheet. The data must be merged with other data files and converted into file formats suitable for analysis. Even when the data is analyzable in a typical spreadsheet, considerable assistance from data analysts who have experience with cost reports is necessary. That is the role and purpose of the People’s Data Project. We prepare and analyze data for nonprofit organizations, legislators, and other Americans who want to understand how money flows through nursing homes, hospitals, Medicaid contractors, and other providers of U.S. healthcare nationally, as well by region, state, county, city, and zip code.

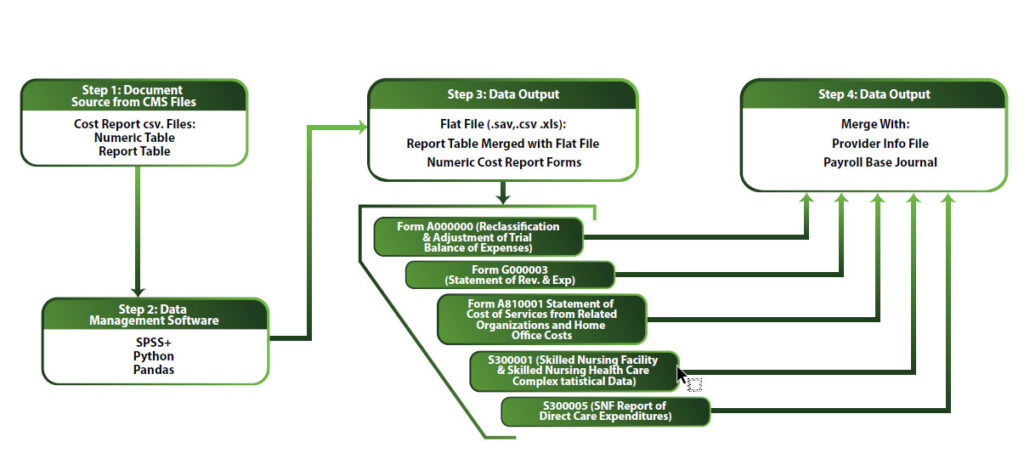

Our data ecosystem has been built with an IBM-SPSS statistical core using Python/Pandas programming languages for file transformation, analysis, and data modeling. Steps in the analytics of hospital and nursing home cost reports are depicted in the schematic below.

This schematic displays the originating sources of data, the tools used to format the data for creating needed output, the necessary organizing structure, and the files the with which data are merged to complete the full picture.

The PDP makes data available online usable for the lay public. In addition, we have extensive experience with and knowledge of hospital and nursing home data and other obtainable healthcare data. Our purpose is to assist nonprofit organizations, researchers, and lay people with obtaining and analyzing data within our bailiwick.

The Dangers of Predatory Corporate and Government Data Analytics are Creating a Democratic Crisis.

Without integrity in the collection and use of data by governments and corporations, Democracy as we know it will disappear. Unfortunately, the power of contemporary corporations with sophisticated technology is producing a crisis of citizen powerlessness. It is also unfortunate that too many professionals and politicians are indifferent to glaring conflicts of interest and intentional misinformation for the purpose of manipulating and misleading the public.

“Without integrity in the collection and use of data by governments and corporations, Democracy as we know it will disappear.”

The data crisis we are facing can only worsen with the advent of AI and increasingly sophisticated data analytics tools. It is despicable for industries to misuse technology and statistics to prey on unsuspecting populations needing healthcare. There is no doubt that AI is a powerful tool that can be used against “We the People.” However, The People’s Data Project will empower people to harness the power of AI and data analytics for fighting back against those forces that are using it against them.