The Scope of the COVID Long-Term Care Tragedy & Lack of an Outcry for Accountability Is Horrifying

Compared to our peer countries in the advanced industrialized world, the United States has been a complete and utter failure in the protection of vulnerable long-term care patients from COVID. At this time, we can only estimate the total loss of life in skilled nursing institutions, but the number of patient deaths has probably reached 200,000.

Except for centuries-long assaults on the health of African Americans and Native Americans, and the flu pandemic of 1918, these deaths comprise the biggest medical tragedy in U.S. history. Certainly, they constitute the most massive loss of life in one demographic group in such a short period of time. If experiences of other countries around the globe are any indication, a large proportion of these deaths were preventable. As I stated in an earlier blog, for instance, S. Korea has had less than 400 deaths from COVID in its long-term care facilities (more about other countries’ COVID losses will be on later posts and one accompanying this post).

An industry was entrusted by the federal and state governments with the care of at-risk elderly and disabled patients. For the most part, the industry failed. In addition to cross-cultural comparisons, evidence suggests that the industry was either incompetent, or greedy, and derelict. Nevertheless, there has been not been an outcry from the public, legislators, and regulatory agencies for accountability through some type of 9/11 commission.

The Industry Is on Offense. But What Exactly Does a Claim of $35 Billion Loss in Revenue Mean?

Passivity on the part of individuals and organizations one would expect to speak out about industry dereliction is not only horrifying, but it has also left the media playing field to the industry. Consequently, the industry’s narrative, based on misinformation and no information, is designed to escape culpability as well as to squeeze a higher level of funding from Medicare and Medicaid.

Having observed industry television interviews, press releases, and print reports in publications such as the New York Times, I am beginning to surmise that the industry’s objective is to depict operators and, consequently, parent corporations, as victims of a natural disaster over which they had no control. Their propaganda ignores preventative measures that could have been taken while it is focuses on exaggerated financial losses.

On February 10th, Alex Spanko reported in Skilled Nursing News that the American Health Care Association (AHCA) had made dire projections of financial losses incurred by the industry throughout the 2020 and 2021:

Nursing facilities will lose a total of $22.6 billion in revenue during 2021, according to a new projection from the American Health Care Association, as occupancy – the primary driver of income for facilities – remains low.

On top of an $11.3 billion decline already seen in 2020, that would brings [sic] the COVID-19 financial toll to $34 billion, or a decline of 24%, even as expenses related to staffing, personal protective equipment (PPE), sit at an estimated $30 billion per year for 2020 and 2021.

Nursing Home Industry Projects $34B in Revenue Losses, 1,800 Closures or Mergers Due to COVI – Skilled Nursing News

Let’s put these claims into perspective. If indeed, total two-year revenue loss of $34 billion could empirically be demonstrated as valid, the impact of that would be de minimis on an industry with revenues of hundreds of billions per year. However, we need to see evidence supporting the AHCA claims.

More importantly, in evaluating corporate financial performance, factors other than total revenue are essential: (1) Net income may still be robust or even higher in conjunction with a reduction in revenue, and (2) Cash flow, the real metric investors are looking for, may actually be improved in a year in which revenue has dropped. Furthermore, skilled nursing is often embedded in corporations in the broader senior housing industry. For instance, real estate investment trusts, private equity firms, and other corporations typically own a broad senior housing portfolio of continuous care retirement communities (CCRCs) in which independent and assisted living are combined with a skilled nursing facility, and stand-alone facilities providing apartment housing, assisted living, and skilled nursing.

I love to listen to Dr. Anthony Fauci speaking on behalf of the Biden Administration these days say, “let’s look at the science, let’s look at the data” regarding vaccines. It is a refreshing change from the previous administration. Hopefully, we can do the same thing when we examine the financial impact of COVID on the long-term care industry.

You Can’t Trust Industry Research Reports

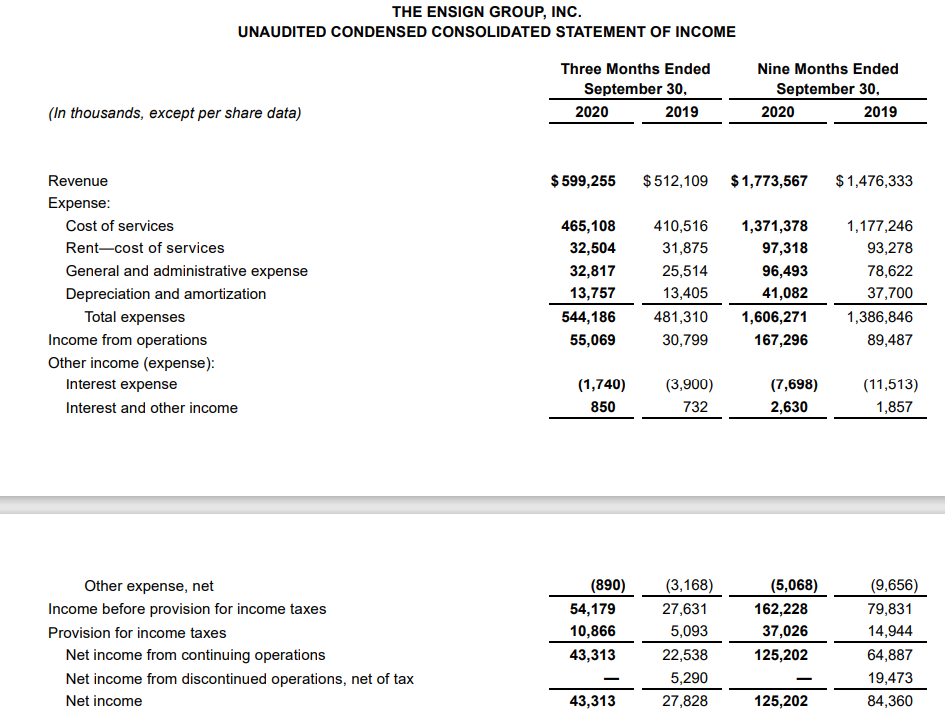

We are lacking sufficient information to substantiate industry claims while at the same time misinformation is distributed across the world of finance. I do not claim to have my mind wrapped around the entirety of the long-term care industry – it is, after all – an industry that operates behind a veil of secrecy. However, the data that I’m collecting suggests that the highly subsidized (maybe most subsidized) industry providing skilled nursing is doing well (see my post re: The Ensign Group today).

“Doing well” is my description of consolidate financial statements, including, but not limited to: revenue growth over a period of years, net income, equity, and cash flow (liquidity, cash/equivalents, lending facilities, etc.).

You can find industry financial information that sells for a very high price. Take it with a grain of salt. For instance, IBISWorld, one of the leading sellers of industry information revealed its analysts’ ignorance of the long-term care industry by claiming that Genesis HealthCare, Inc and HCR ManorCare are the “biggest companies” in the “nursing care facilities industry in the U.S.” Beside that claim is a red lock icon, which means if you pay an excessive fee, you can see the data backing the claim (https://www.ibisworld.com/united-states/market-research-reports/nursing-care-facilities-industry/).

. Don’t waste your money. Genesis is a zombie company that probably won’t survive much longer and has been reduced to a contract managing firm – its property and operating entities are now owned by a Real Estate Investment Trust (REIT). Like Genesis, HCR ManorCare was bankrupted by a private equity firm and its property was sold to a REIT. These companies don’t represent the industry and analysts indicating that they do are providing bad information.

By Dave Kingsley