By:

Dave Kingsley

American Tolerance of Corporate Deceit & Predatory Economics is Perplexing

Misinformation can be harmful and even deadly. We have seen evidence of this maxim during the COVID crisis. We have seen it in the debate over climate change and in so many other critical issues confronting society. In post-truth America, it has become acceptable to put forth any mistruth or unverified and unverifiable claim and escape embarrassing denunciation, excoriation and censure. In no case is this more apparent than in the mistruths spread by for profit corporations in the nursing home business.

It isn’t difficult to compile objective evidence that nursing home industry hardship pleas of low profits, thin margins, and other such claims are false and misleading. The American Health Care Association/National Center for Independent Living, the industry’s lavishly funded propaganda organ, consistently spreads the narrative that corporations in the Medicaid and Medicare funded long-term care business are struggling financially and need a significant increase in reimbursements.

A highly qualified financial sleuth isn’t needed for debunking the industry’s financial narrative of low profits and struggling investors. Therefore, it may be difficult to understand how nursing home reform commissions and politicians escape public opprobrium for ignoring the patently obvious. However, it should be understandable that the finer points of nursing home finance isn’t on most peoples’ radar. We need to put it on everyone’s radar.

The Nursing Home Industry is Lying to the American People and Getting by with It

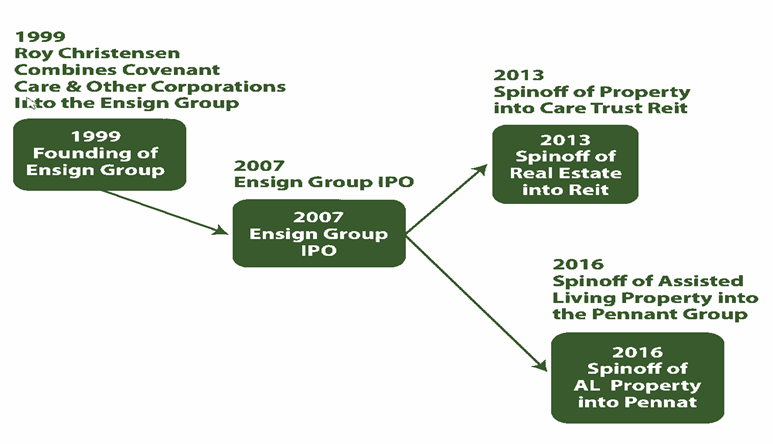

The truth is that the federal and state governments allow for a charade in which facility-specific costs are submitted without any clarity about cash flowing to holding companies and parent corporations. We don’t really know how much Medicaid and Medicare revenue in the privatized nursing home system is extracted for dividends, and executive pay. ONE BIG EXCEPTION, HOWEVER, IS THE ENSIGN GROUP.

With an annual revenue in 2022 of over $3 billion, the Ensign Group is the largest single provider of nursing home care in the United States. It is also the only publicly listed company that earns revenue solely from Medicaid and Medicare funded long-term care. More importantly for understanding the financial realities of the nursing home business, it is a publicly listed corporation and therefore must file financial reports with the Securities & Exchange Commission (SEC).

The Ensign Group annual 2021 10-K report submitted to SEC notes a net income of 8.5 percent and earnings before interest, taxes, depreciation, and amortization (EBITDA) of 13.7 percent. However, an examination of their six facilities in Kansas reveal a combined net revenue of $55,567,680 and a combined operating negative net of -3,201,123 (-5.7%). Five of the six facilities reported a negative net income.

Facility-Specific Cost Reports: How the Big Lie Works.

A review of Ensign Group cost reports in one state, i.e., Kansas, provides insight into how the misleading state-specific and facility-specific financial system works. Ensign operates six facilities in the state of Kansas. Comparing the facility-specific cost reports to the consolidated financial report submitted by Ensign to the SEC is instructive in demonstrating the inadequacy of the cost reports as a measure of financial performance.

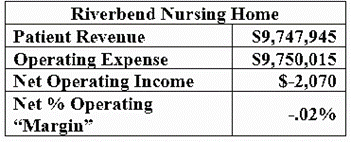

For instance, Table 1 contains cost report data from an Ensign owned facility known as Riverbend Nursing Home in Kansas City, Kansas (incorporated and licensed as Big Blue, LLC). The data indicates that the facility, with a slight negative net operating income, lost money (this is 2021 data). It is typical for facility cost reports to show a very low or negative income but that doesn’t reflect what parent corporations are earning from the operations.

Table 1: Net Operating Margin

Form CMS 2540-10: Home Office Allocation & Related Parties

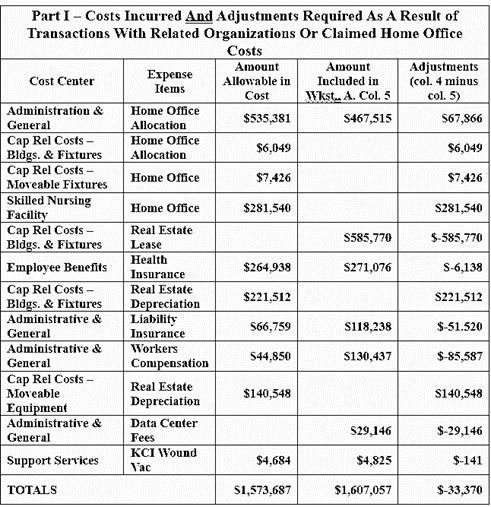

Parent Corporations with a chain of facilities incorporated as LLCs can claim an allocation to their home office based on corporate expenses for operating each facility. The “home office allocation” appears to be a large allowance for expenditures that are not fully clarified, not decipherable by the public, and, I believe, not understood by state auditors. For instance, Table 2, includes claims for Ensign home office allocation and payments to their subsidiaries paid for insurance and real estate.

Table 2: Part I, Riverbend Form CMS 2540-10

Corporate Hubris: They Don’t Need to Answer Questions Required by Law

A state auditor with whom I had a conversation recently asked me if I had any insight into the home office allocation that might be helpful for auditing purposes. This person knew that I had been looking at cost reports across the U.S. and thought practices in other states might be something of a guide. That the auditor wasn’t sure about how to evaluate funds extracted from revenue and sent up the chain of LLCs (often shell companies) to home offices tells us much.

The auditor is in fact not the problem. Statutes governing Part I of Form CMS-2540-10 (42 CFR 413.17) states that “such cost must not exceed the amount a prudent and cost conscious buyer would pay for comparable services, facilities, or supplies that could be purchased elsewhere.” Commonsense suggests that pricing goods and services sold to related parties requires some sophisticated and extensive analyses. Do states have the regulatory capacity to do that? Advocates and scholars need to raise that issue with legislators and demand to see any evidence supporting decisions to approve claimed expenditures to related parties.

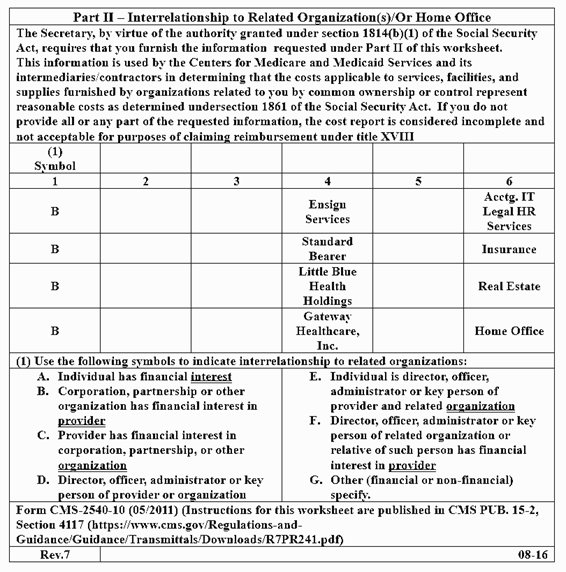

Part II of Form CMS 2540-10: How Vague Can They Be?

Part II of Form CMS 2540-10 requires far more detail than shown in Table 2, which reflects the exact data submitted by the Ensign Group for its facilities. For instance, the statute requires that an entity listed in Column 4 “enter a percent of ownership in the provider.” That may not be a logical question because Ensign corporate owns everything. Gateway Healthcare is a shell company that merely hides the flow of capital, avoids taxes, and protects the facility from liability. Theoretically, Gateway owns 100% of Riverbend, but Ensign owns 100% of Gateway (an LLC incorporated in Nevada).

Therefore, Ensign’s facility-specific cost reports merely ignore statutory reporting requirements. That appears to be acceptable to state auditors. This kind of “catch us if you can” hubris is typical when an industry has an extraordinary amount of money to spread around in Washington and the 50 state legislatures.

Table 3: Part II, Riverbend Form CMS 2540-10

Summary: CMS Allows States to Regulate Nursing Homes & Looks the Other Way

CMS is not likely to fix the corrupt and inadequate nursing home financial reporting system. They will noodle with advocates and mull over all sorts of well-founded and sensible proposals but without pressure from legislators to counter the industry’s power in Washington and in the 50 states, the status quo will prevail.

The political will just isn’t there at the national level. We need to change that. Advocates are likely to make more progress at the state level by compiling cost reports in their respective states and take their analyses to the media and state representatives. The critical – life and death – nature of this problem should lead the public to revolt if they understand it and have the evidence to clearly see that the industry narrative is false.

Lack of staff and poor quality of care leads to shortened lives and considerable suffering. That could be fixed by stopping the excessive extraction of cash sent up the line to investors and executives. That will only be stopped by a narrative based on verifiable fact and a coordinated effort to spread that narrative in the media and among state legislators. Financial data may not seem interesting on the evening television news or in the print media. But we are obligated to make it understandable, interesting.